Paying for Unexpected Feed Expenses

by Tom Anderson

Introduction

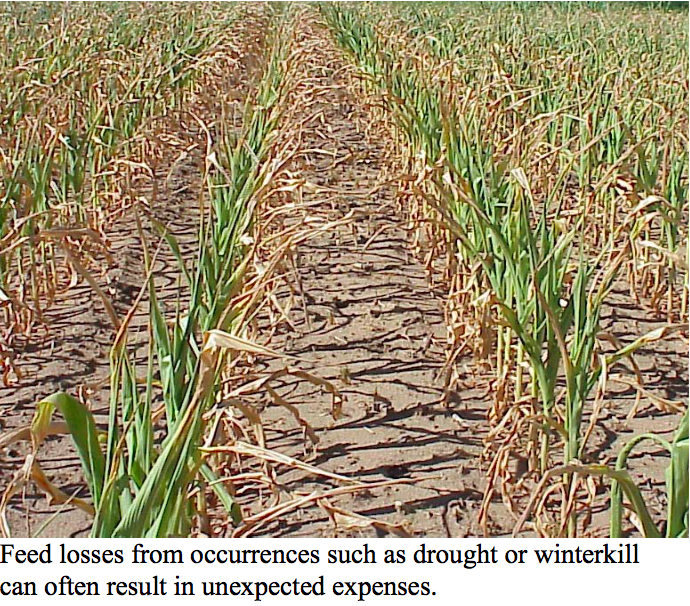

There are times when crops fail. Drought, winterkill, and flooding are beyond our control. When these conditions combine with low commodity prices, they present a special challenge to the farm checkbook. What follows are some thoughts from agricultural lenders about securing credit to bridge unexpected expenses.

How does a farm operator take advantage of cash discounts, meet unexpected costs, and stay current on existing accounts to preserve a good credit rating?

While some farmers pay cash, an operating loan is the most common way to meet annual occurring expenses such as feed, seed, fertilizer, fuel and taxes. Operating loans are structured as closed end or open end lines of credit. Many lines of credit will automatically extend credit to your checking account. This saves the bother of frequent trips to the bank, and might save the cost and embarrassment of checks returned due to insufficient funds.

What are the repayment terms for operating loans?

Repayment terms for operating loans vary by lender. Some lines of credit are to be repaid with monthly payments over 12 months. Other lines of credit require a set percentage of the principal be repaid each month. And still other lines of credit require the interest be paid each month with the principal to be repaid some time during the year as the borrower has the ability to pay.

Do farm operations need collateral for an operating loan or a line of credit?

In most cases, livestock, machinery or the crop to be grown, harvested, and sold secure operating loans and lines of credit. In a few cases, it is possible that an unsecured line of credit could be extended to farm operators if the farmer provides financial statements that demonstrate financial stability and has an excellent credit history.

What are the options for additional operating credit if existing collateral is already pledged on other loans?

At this point, your options are limited. You can seek point of purchase financing from the seller or vendor of the seed, fertilizer, or feed you are buying. You may also request that your existing lender look at restructuring your debt, or shifting some of your debt to other collateral. Finally, you might explore the option of refinancing with another lender.

My alfalfa winterkilled and additional feed needs to be purchased. What if this unexpected operating loan results in a negative monthly cash flow?

My alfalfa winterkilled and additional feed needs to be purchased. What if this unexpected operating loan results in a negative monthly cash flow?

You may have to ask your lender to treat your operating loan request as an extraordinary occurrence. That may allow for a longer payback period than one year. While it is true that amortizing your operating expense over several years will improve cash flow, it is not a good practice to follow except in a true emergency. In extreme cases, you may need to pledge additional collateral such as land to secure operating capital.

What’s a good approach for working with an agricultural lender?

Establish a routine of getting your annual line of credit worked out as early in the year as you can. Once you have your farm earnings statement and updated balance sheet, make an appointment with your lender. This should happen no later than March. Then if you need access to additional funds contact your lender as soon as you are aware of your need for new credit. Be prepared with your specific request. The turn around time for approval will vary from one day to three weeks.

Are there any state or federal loan programs that exist for emergencies?

Wisconsin has a WHEDA CROP program for financing certain operating expenses such as feed. The loans range from a minimum of $2000 to a maximum of $60,000. These loans are guaranteed to the lender. The maximum interest rate is the prime rate plus 1%. A non-refundable application fee of $200 to $400 is charged and can generally be included in the loan. To qualify, your debt to asset ratio must be greater than 40%. These loans are commonly secured with the crop or the feed being financed. WHEDA loans are to be repaid by March 31st of the following year. WHEDA loans are accessed through your agricultural lender.

The USDA Farm Service Agency provides direct loans and, from time to time, federal emergency loans. Contact your local FSA office to see if there is an emergency loan program or direct loan program available to meet your needs. Farm Service Agency also has programs for guaranteed operation loans and line of credit programs. Contact your agricultural lender for details about these guarantee programs.

Thanks to Dave Kappelman of Premier Community Bank and Gary Luethi of Greenstone Farm Credit Services for their input in developing this “Focus on Forage”.

![]() Focus on Forage – Vol 5: No. 3

Focus on Forage – Vol 5: No. 3

© University of Wisconsin Board of Regents, 2003

Tom Anderson, Agricultural Agent, Shawano County

University of Wisconsin – Extension

UWXTOM@co.shawano.wi.us