March 2022 — Housing is an essential element in the revitalization of downtown districts. Demographic and lifestyle changes create new opportunities for specific residential segments and housing categories. This section provides an abbreviated method for assessing general market opportunities using a simple demand and supply analysis for a community. A more focused assessment of downtown housing opportunities is then discussed.

A healthy downtown residential district generates a constant flow of foot traffic to support nearby retailers, services, restaurants, and other businesses. The concentrated mix of retail, office, and entertainment typical of a downtown puts residents within walking distance of most daily activities. Living downtown is particularly attractive to many who work downtown. By incorporating a higher density of residents in the downtown mix, the amount of activity increases. This in turn creates an even more vibrant, desirable downtown economy.

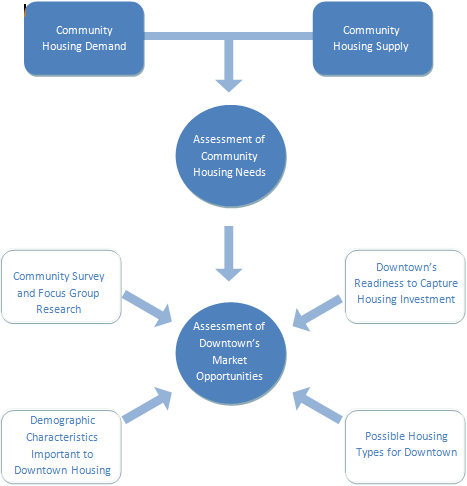

This section will help you assess community housing needs in the larger area, and then identify specific market opportunities appropriate for downtown. A flowchart that illustrates the components of this analysis is presented below.

Community Housing Demand

Current and projected demand for housing depends in part on both demographic characteristics and economic conditions. Demand is measured in housing units of all types including both rental and owner-occupied.

The first step is establishing a community-wide housing market area that (includes and extends beyond the downtown area. This is defined as the area in which housing units compete with each other. It might include the city, village, county, or other census-designated geographic area. The housing market area will often be influenced by population density, school-district boundaries, transportation linkages, shopping and service linkages, and distance to major employers. It is likely that the housing market area will be different from the trade area defined for retail and other businesses and presented earlier in the toolbox.

The following types of information should be analyzed to understand historical and projected changes in demographic and economic factors that will impact housing demand. Much of this information may have already been collected in early parts of the market analysis. The forms in Appendix A can be used to assemble data for your community.

Population and Households. It is important to gather accurate data describing your community’s population trends. Is the number of local residents increasing or decreasing, and at what rate? Which segments of the population are changing the most? Since the demand unit for housing is the household, it is critical to obtain information on the characteristics of the community’s households. For example, if household sizes are shrinking but population is stable or increasing, then there will be demand for a greater number of housing units and possibly units that are smaller. Accordingly, information (historical, current, and forecasted) should be gathered on population and households including size and type.

Age. Generational differences will translate into different housing priorities. For example, householders under 24 years old may feel that home ownership is not a priority, but affordable rent, access to high-speed internet, and proximity to arts and entertainment are important in their housing choice. Accordingly, it is important to understand how age categories in your community have and will change in coming years.

Income and Employment. Understanding local income levels is important in planning for housing needs because income determines the type of housing that people can afford. The strength and characteristics of the employment base should be examined and related to the population, household, age and income assumptions. If possible, a survey of major employers in the area, including expansion plans, reductions in force, relocations, and any new employers entering the area should be part of the information presented. Demand for new housing is often closely tied to workers moving into an area. Data on household income and occupations for the market area should be collected and compared with the state to determine how the local area is different.

Data for analyzing current and projected housing demand in your community can be obtained from the U.S. Census Bureau, private data firms, community and regional planners and other sources. In Wisconsin, GetFacts is a project of UW-Madison’s Applied Population Lab and UW-Extension. The website lets you create and tailor your own census profiles, includes housing information, and is fairly simple to use.

Move-Up and Latent Demand. The market area may also have move-up or latent demand. Move-up demand is generated by the upward mobility of lower-income households. Move-up demand can sometimes be identified if the rent-to-income ratio for certain lower income groups is low relative to historic trends and comparable communities.

Latent demand, also called pent-up demand, typically results from under-building in an area. If for example, over the last few years, apartment buildings had not kept pace with the population increase and an increasing rental market, latent demand might be present. Accordingly, latent demand can be analyzed by studying the types of housing that your major market segments are choosing in comparable communities.

Real estate professionals in your area can provide insight on move-up and latent demand in your community.

Community Housing Supply

The current supply of housing units provides a basis for assessing the future availability of housing. In order to understand the nature of a community’s housing stock, information about size and characteristics of existing housing units must be gathered and compiled. For the community-wide housing market assessment, the following types of information must be collected. The forms in Appendix A can be used to assemble data for your community.

Number and Type of Housing Units will quantify the number of housing types including single-family detached homes, duplexes, multifamily structures, and mobile/manufactured homes. If possible, the housing supply data should be broken down into segments consisting of different types of uses, quality, and affordability.

Tenure refers to whether the housing unit is owner-occupied or rented by the occupant. Information on tenure is important because the community should have a sufficient supply of units to satisfy the needs of both renters and owner-occupants.

Vacancies provide a count of the number of housing units that were vacant and available for rent or sale. The vacancy rate (the number of housing units vacant and available divided by the total number of units) is an important measure of whether the housing supply is adequate to meet demand. It is important to note that some vacancies are necessary for a healthy housing market. According to HUD, an overall vacancy rate of ~3% allows consumers adequate choice. For owner-occupied housing, an acceptable rate is 1.5% and for rental housing it is 5%.

Housing Prices refers to the price of owner-occupied housing. The median price, as it varies over time, is an indication of housing demand. It is equally important to know the distribution of housing of different values.

Rental Rates refers to market rents for housing. It is important to track the number of rental units available at different rents as an indication of the availability of an adequate supply of rental housing for different income groups in the community.

In addition to the data above, local real estate trends should be collected. This can include the condition of current housing stock, construction trends, time-on-the-market, absorption rates, and subsidized and special-needs housing. In addition, information on any new projects should be collected including location, number of units, type, size, and rent or sales price.

Data for analyzing current and projected housing supply in your community can be obtained from the U.S. Census Bureau, private data firms, community and regional planners, and other sources. Updated vacancy data can usually be obtained from assessors, homebuilders, realtor associations, and rental management groups. Contact apartment owners and associations for rental rates. Real estate multiple listing services (MLS) and homebuilders associations can provide data on home prices. Conversations with sales agents, appraisers and mortgage brokers are useful for gauging trends in home selling prices. Newspaper house and rental listings also provide useful information in estimating housing costs.

Assessment of Community Housing Needs

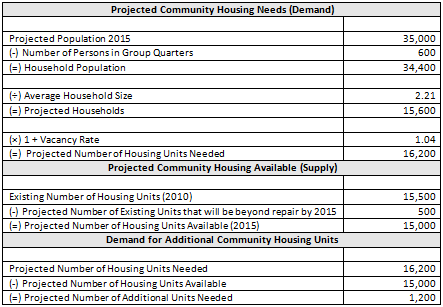

The projected number of additional housing units needed in the community-wide market area can be approximated through a simple model. It is based on the data provided earlier for examining community housing demand and supply. The following exhibit provides an example of how to calculate the future need for additional housing units in your community. The forms in Appendix A can be used to develop this projection for your community.

The previous calculations provide a preliminary analysis of demand and supply conditions in the community-wide market area. A more comprehensive and refined housing study for the entire community would be needed to address specific housing issues such as:

- How do factors such as school quality and tax rates affect demand for housing in the community?

- Is rehabilitating existing housing stock more important than creating new housing?

- Is adding rental housing more important than adding owner-occupied housing?

- For what income groups is housing most needed?

- Does housing stock reflect the needs of a maturing and aging community?

- Does housing stock accommodate the needs of persons with special needs?

- Will there be changes in household size due to in-migration or to the growing population of elders?

These important questions are beyond the scope of this preliminary assessment. However, the guidelines for preparing a more comprehensive community housing plan (identified earlier in this section) are available to guide you in this process.

Assessment of Downtown’s Market Opportunities

Before additional market analysis specific to downtown housing is conducted, it is important to step back and examine whether your downtown is ready to pursue new housing development. For your downtown to be an attractive place to live, it must be an attractive, mixed-use environment for living, working, shopping, and entertainment.

A paper prepared for the Brookings Institution titled Ten Steps to a Living Downtown describes two preconditions for successful downtown housing efforts.

- The physical environment must be of a character and quality that people will want to live there. Downtown must be perceived as a comfortable and safe place. It should have boundaries, be of human scale, and have clusters of housing that are obviously distinct from businesses. Neighborhoods must provide places to play, direct access to food shopping, services, and neighbors. Downtown neighborhoods must be clean, and must above all be safe from threats and crime.

- Downtown residences must offer an investment motive for home ownership. For downtown housing to take root, people must be willing to purchase their homes, not just rent. For this to happen, they will have to have confidence that they will eventually be able to sell for a higher price than they paid to buy. Like the suburbs, downtowns must meet at least these two conditions – be a safe, quality environment and provide investor confidence – before they can effectively compete for residents.

The paper also offers steps city officials and others can take to foster a living, 24-hour downtown. These steps outline ways that local public policy might strengthen the two threshold conditions – a strong quality of life and market conditions – that are necessary to attract residents to central business districts. The complete paper, Ten Steps To A Living Downtown: A Discussion Paper.

Survey and Focus Group Research

Survey and Focus Group Research can be a useful step in evaluating residential opportunities in your community. This type of research provides information on how people perceive the quality of life downtown, the importance of various housing amenities, and the desire to rent or purchase. Specific market segments can be targeted, such as downtown employees or existing community residents.

Surveys, while expensive, can be very useful in determining resident’s feelings towards downtown housing. The answers can be used to adjust your housing plan, and can be given to potential developers who are in need of information regarding resident’s preferences. The following are questions to include.

- If you moved or stayed downtown would you prefer to rent or own? This question allows you to examine your housing mix and work to develop new housing that meets the demands of potential and current housing consumers.

- What type of downtown housing is most attractive to you? This question allows you to determine what types of housing (condos, apartments, townhouses, etc.) should be built and adjust your housing plan accordingly.

- What size housing unit do you require? The answer to this question will help you determine if the current housing options (# of bedrooms/# of bathrooms) meet the needs of potential residents.

- Do you prefer historically renovated or newly constructed buildings? This will help determine if historical buildings should be converted into living units instead of office or retail space.

- What features/amenities are important to you? Knowing what amenities are desired (AC, dishwasher, parking, washer/dryer, etc.) will help you compete with other housing options in the community and allow you to tailor your housing projects to meet the needs of potential and current residents.

Conducting focus group research is an important way to enhance the findings from a survey. Focus groups allow participants to share information that they may not have been asked about in a survey. This allows you to obtain an in-depth understanding of consumer preferences. Areas that participants could be asked about include project locations, housing amenities, design issues, purchasing motivation, and financing options. For more about conducting a focus group, please see the focus group section of the toolbox.

It is important to conduct a few focus groups aimed at different markets. For instance, one would be aimed at current residents of downtown with the purpose of determining what areas need improvement. The second group would target potential residents who may be considering moving downtown. This group would seek to determine what amenities and housing options are needed to attract new residents to the downtown area.

Demographic Characteristics Important to Downtown Housing

While many community residents may desire single-unit homes, national trends have moved towards smaller households. The household mix now includes a variety of non-traditional family and non-family forms.

As the dynamics of the population change, different types of housing units are needed. Also, as householders progress through time, or a life-cycle, their individual housing needs also change. Not only do children move out, but aging homeowners retire as well. This often results in the increase of demand for condominiums and high-end rental units. Finally, household income levels also change with time. Changes in Income levels will affect the type of housing demanded. All of these factors create movement within the housing market.

The housing industry will have to cater to an increasing range of needs and preferences as demographic changes occur at both the national and community level. Listed below are the needs and preferences of specific market segments as they relate to downtown housing. These segments need to be analyzed in relation to the community demographic data analysis presented earlier in this section. Those segments which are growing in your community and are most inclined toward downtown living (downtown workers, singles and couples without children) should be included in your assessment of downtown housing opportunities.

Householders less than 24 Years Old

A number of householders less than 24 years old are upwardly mobile professionals with high household incomes. Some may be employed in the downtown area, and others include college students (married and single) attending nearby campuses. Many householders less than 24 years old are in the rental market, or just moving on to homeownership. Householders less than 24 years old tend to have many of the same characteristics generally attributed to householders between 24 and 35 years old.

Many aspects of downtown living are attractive to this group. They are willing to trade space for convenience and the diverse neighborhood character. Additionally, this group is much more flexible in terms of location, as they are technically savvy and often have the option to work from home. Downtown apartments on upper floors over retail, and live-work units are likely to be attractive to this group. Downtown workers in this segment are key prospects for downtown housing. This substantial market segment is making its presence felt in the residential market, and downtown has a lot of the amenities they are looking for in a community.

Householders 24-35 Years Old

Householders 24-35 years old have long escaped the attention of the real estate industry. Members of this generation are more likely to be individualistic, driven professionals that work long hours, have significant disposable incomes, and are very focused on lifestyle choices. Furthermore, they express a strong inclination towards home ownership.

One clear trend among this age group across the country is their willingness to sacrifice space for convenience. They prefer live-work units, flats, and condominiums in infill locations close to work and services. Location is clearly an important factor in their decision to rent or own a home. Essentially they want their daily needs met a short distance from their doorstep. Householders 24-35 years old that have yet to start families and appreciate an urban atmosphere, convenience and entertainment amenities are likely consumers of downtown housing. Again, downtown workers in this segment are key prospects for downtown housing.

Householders 36-55 Years Old

Householders 36-55 years old have been the defining market segment for over half a century. As they get older, they are expected to redefine what are considered typical preferences for the empty-nester/retiree age group. In addition to this, they don’t see themselves as ‘older’ until their upper 70’s, and will not make lifestyle or housing choices that appear geared towards old age or slowing down. This group appears much more predisposed towards convenience and an urban lifestyle, with more compact living quarters, than previous generations. A growing number of 36-55 year old householders are looking for the flexibility and cultural offerings of a city center.

Householders 36-55 years old are more likely to own than to rent, though there will be some demand for rentals from those who want the option to move away if the lifestyle does not suit their needs. Many will require spaciousness or the illusion thereof, state-of-the-art home amenities, and nearby recreation. A downtown that puts daily activities within walking distance ensures a greater level of independence as they age. Furthermore, historic downtowns that offer civic and cultural amenities and opportunities to engage in community activities will be especially attractive to this market. Again, downtown workers in this segment are key prospects for downtown housing.

Householders 56-69 Years Old

Householders 56-69 years old are a group whose children have typically moved out of their home. As a result, they live in a home that is too big for their needs and are looking to downsize. In addition, they often do not care to deal with the maintenance of a home as they age. People in this segment are moving towards retirement and are looking for a sense of community with ample entertainment options to fill their free time. It is also important to note that without dependents, this age group typically has high disposable income.

Downtown condominium units have been popular among householders 56-69 years old because they are able to walk to coffee shops, restaurants, stores, the library, theaters or the civic center. Overall, this group is looking for a place where they are able to enjoy life and increased leisure time without dealing with the maintenance of their homes. Because this is a large segment, a modest percentage of householders 56-69 years old moving downtown would add significant demand for downtown housing.

Householders 70+ Years Old

Householders 70+ years old can be segmented into elders living independently and elders utilizing supportive services. Those living independently are, “disproportionately married couples in good health and with middle-class incomes,” while those utilizing support services are generally over 75 years of age and may have lower incomes.. These groups are less likely to live in large cities or suburbs. Rather, many prefer non-metropolitan areas such as small towns and retirement destinations.

Retirement housing options reflect a hierarchy of needs. They include active adult units (targeted to elders living independently), congregate care (limited assistance with transportation or meals), assisted living (for elders requiring additional services), nursing homes, and continuing care retirement communities (mixture of senior housing types). Rental retirement housing demand will increase as the householders of the area age. Depending on income levels, retirement households will also increase the demand for condominiums.

Possible Housing Types for Downtown

Downtown housing developments typically involve utilization of existing buildings, as well as infill projects to create a higher density residential neighborhood. Best practices in downtown housing include rental and owner-occupied units reflecting rents and prices that serve all segments of the market. The following are some of the general categories of downtown housing that exist in small cities:

Upper-Floor Units – These units are often located on the upper-floors of downtown stores, offices, restaurants, and other businesses. Most are rented out, but sometimes the unit is occupied by the building owner or operator of the first-floor business. These units can offer low-rent options for those who require affordable housing.

Townhouses – Townhouses provide the amenities of a house in a downtown setting. Most townhouses share common walls, so a significant number of units can fit onto a small city lot. They attract people who do not want to live in an apartment-style unit but do want to live in or near downtown.

Apartment or Condominium Building – These freestanding buildings can bring significant population density downtown and can serve those looking for rental units or owner-occupied units. By offering convenience and center-city amenities that are not available at other apartment/condominium buildings in the area, downtown housing can gain a competitive market advantage.

Live/Work Units – These units allow the occupant to comfortably live and work in the same unit. They are appropriate for a number of service businesses that are run from the home and help the tenant save on renting an additional office. For those residents intending to work from home or telecommute, live-work units provide office space, or even a small business under one mortgage. These units are also appropriate for artists and artisans. Having these units downtown will help attract entrepreneurial-minded residents.

Loft Units – Loft units are created by converting former office, industrial or warehouse space into apartments or condominiums. These units offer unique spaces that are sought by downtown residents and provide a good way to rehabilitate older or unused buildings downtown.

The process of incorporating housing into the downtown mix will involve an assessment of the amount of demand for these types of units, as well as the analyzing the current supply. Understanding the dynamics of the local market will be the basis of such an analysis. Finally, the placement of such units will require an assessment of housing’s compatibility with other downtown uses (see the Space Utilization section of the toolbox).

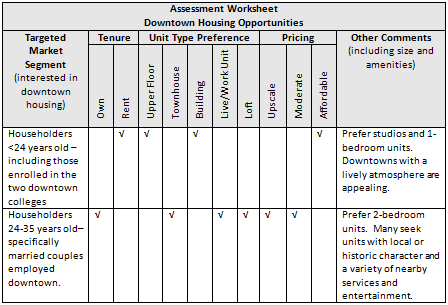

Assessing Downtown Opportunities Worksheet

Your assessment of downtown housing opportunities should be summarized in specific recommendations regarding housing types that make market sense. The following exhibit provides one way to organize the findings from your housing research and identify what types of units (tenure, type and pricing) would appeal to key market segments.

Use the blank form in Appendix B to complete the Downtown Housing Assessment.

- In the Target Market Segment column, list those market segments (i.e. Householders less than 24 years old”) that may be attracted to the downtown and are growing or have existing latent (pent-up) demand. Expand your description of each segment to fully describe important sub-segments (i.e. college students) within your community.

- In the Tenure, Unit Type Preference and Pricing columns, place a checkmark in the columns reflecting the housing preferences of each target market segment. Base your answers on the market segments and insight of local real estate professionals.

- Finally, add any additional comments that describe other preferences of each target market segment including size, specific features, and amenities. Include comments on how well a downtown location would appeal to each segment. Use your local survey and focus group research as well as the insight of local real estate professionals.

About the Toolbox and this Section

The 2022 update of the toolbox marks over two decades of change in our small city downtowns. It is designed to be a resource to help communities work with their Extension educator, consultant, or on their own to collect data, evaluate opportunities, and develop strategies to become a stronger economic and social center. It is a teaching tool to help build local capacity to make more informed decisions.

This free online resource has been developed and updated by over 100 university educators and graduate students from the University of Wisconsin – Madison, Division of Extension, the University of Minnesota Extension, the Ohio State University Extension, and Michigan State University – Extension. Other downtown and community development professionals have also contributed to its content.

The toolbox is aligned with the principles of the National Main Street Center. The Wisconsin Main Street Program was a key partner in the development of the initial release of the toolbox. One of the purposes of the toolbox has been to expand the examination of downtowns by involving university educators and researchers from a broad variety of perspectives.

The current contributors to each section are identified by name and email at the beginning of each section. For more information or to discuss a particular topic, contact us.